Background

Technologies developed in 2013 and promoted by ExxonMobil, together with joint venture agreements between Saudi Aramco, CB&I (now McDermott) and Chevron Lummus (CLG) have resulted in the commercialisation of Thermal Crude to Chemicals, TC2C™ technology, also (sometimes) known as Crude-oil-to-chemicals (COTC).

A conventional refinery’s primary goal has been the production of transportation fuel (diesel, gasoline, aviation fuel) with many petrochemicals produced as side streams during crude oil refining.

The energy transition is shifting the drivers of oil demand towards petrochemicals, making refinery integration an important growth strategy for oil companies. An integrated refinery is one where refining and petrochemical units are interconnected, often on adjacent sites. This approach is designed to make refinery operations more sustainable. The conventional model, where refiners generate revenue primarily by processing crude oil to produce transportation fuels, is increasingly under threat from falling fuels demand, particularly in Europe.

Crude Demand and Energy Transition

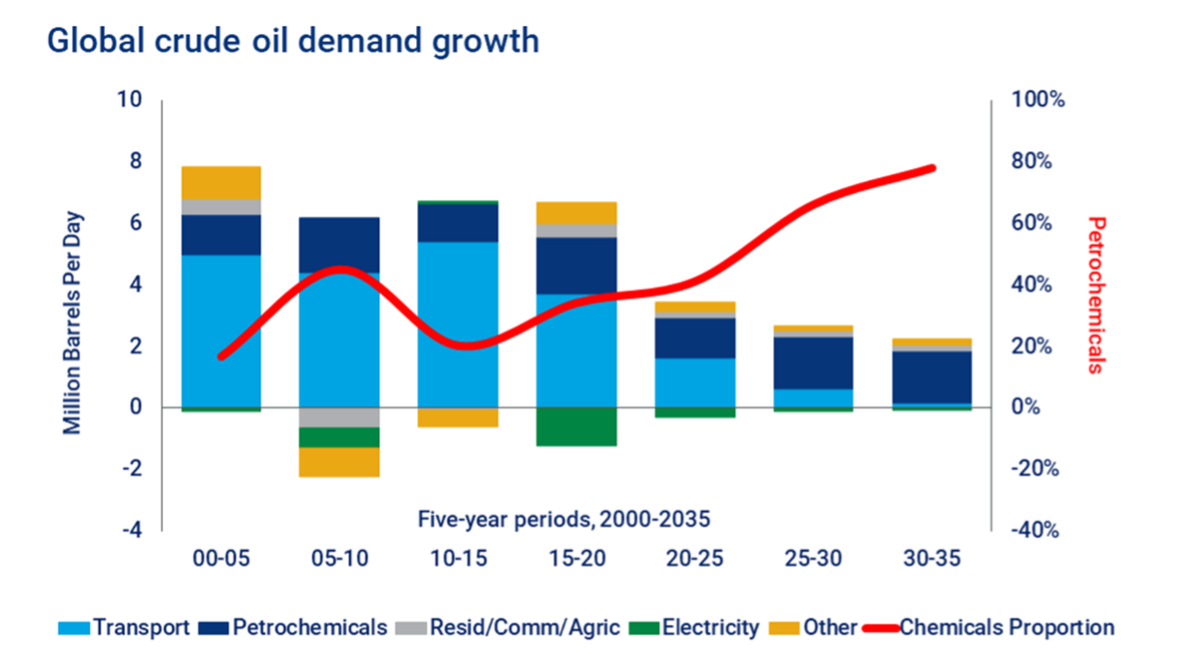

Transportation (fuel) demand currently represents the majority of end-use for crude oil. But as the energy transition progresses – and drives the electrification of transport – that is changing. Petrochemicals used in daily life are now the fastest-growing share of the barrel.

Many oil producers and refiners are shifting their attention to chemicals, particularly olefins and aromatics, as a key target area for the future. Dedicated COTC technologies are being developed and many traditional refineries are exploring retrofitting or building new complexes to maximise production of chemical feedstocks.

This trend will add significant olefin and aromatic capacity, and likely lead to national and international oil companies steadily increasing their stake in the petrochemical market.

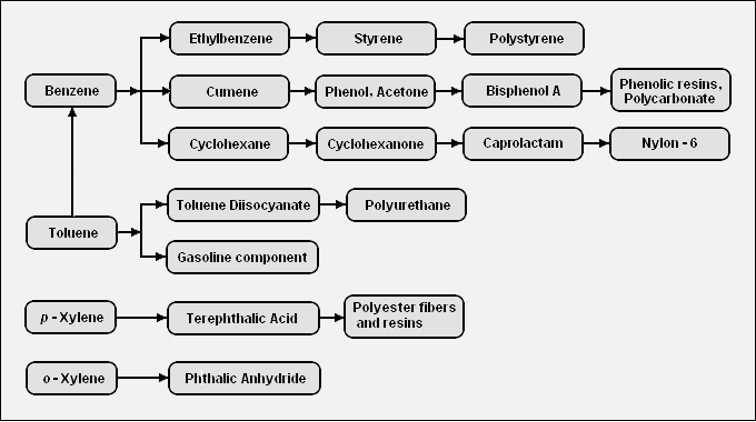

Crude oil has long been used as a direct feedstock in steam crackers to yield olefins (ethene, propene, butenes and butadiene) and aromatics (benzene, toluene and xylene). These high value chemicals are the basic building blocks for a wide range of materials such as solvents, detergents, and adhesives.

Olefins:

The basis for polymers and oligomers used in plastics, resins, fibres, elastomers, lubricants, and gels. In 2019, global ethylene production was 190 million tonnes and propylene was 120 million tonnes.

Aromatics:

There are a large number of petrochemicals produced from the BTX (benzene, toluene and xylene) aromatics. The following diagram shows the chains leading from the BTX components to some of the petrochemicals that can be produced from those components:

However, the direct steam cracking of crude oil, without any pre-fractionation of the crude oil, results in excessive volumes of heavier products which are difficult to vaporise and have high coking rates, resulting in higher frequency of de-coking cycles, increased maintenance costs and lower olefin yields.

As will be seen below, the economic advantage of extracting more high quality and high value intermediate products from each barrel of crude oil drives the COTC technology advancement.

Economics

Most refineries convert approximately 5-20% of incoming crude oil to chemicals, while new COTC technologies aim for outputs in the range of 60-80% of chemicals such as olefins, aromatics, glycols, and polymers.

Whilst the economics of COTC is dependent on the composition of the feedstock and the extraction costs of each barrel of crude oil, the attractiveness of this method appears to reside in countries with low extraction costs, such as Saudi Arabia, Iran and Iraq.

The global chemicals demand is growing at a much higher rate than fuel demand, so the desire to produce higher value chemicals from lower value feedstocks is driving tremendous interest in the new conversion methods.

Likewise, economic volatility in refining margins is a significant impediment to financial planning whilst COTC provides a much more predictable potential. COTC process also gains sustainability with respect to refining/petrochemical traditional processes by reducing the overall carbon footprint of a facility due to integration and optimisation of assets.

"Most refineries convert approximately 5-20% of incoming crude oil to chemicals, while new COTC technologies aim for outputs in the range of 60-80% of chemicals such as olefins, aromatics, glycols, and polymers."

The Future of COTC

There are three degrees of COTC. The first generation is the ‘traditional’ refinery-chemical integration. These sites still focus primarily on fuel production, with chemical yields at 15-20%. Second generation complexes are now targeting up to 40% chemical yields. The third generation will tip the balance to 70-80% chemicals yields, but the technology for this is not yet fully mature.

Integration of specialised COTC technologies into the refining process adds value in several ways. It’s an opportunity to integrate resources, optimise allocation of resources and feedstocks, and share utility, logistics and energy costs. It can also allow a producer to switch product yields between refining and chemicals, depending on where the greatest value lies at the time. All of this can help to reduce cost and improve overall profitability.

The benefits of integration – and the value created – will vary by site, technology choice, complexity, and scale.

We can look to China to see how the second generation is performing. China launched a new wave of integrated refinery and petrochemical investment after the oil price collapsed in 2014-15 and crude import licences and quotas opened to private companies.

In 2019, Hengli Petrochemical’s complex in Dalian became one of the first of the resulting mega-projects to come online. The project features large scale, oil refining at 20 million tonnes/year, with up to 31 major refining units.

Source: www.news.cn

The Hengli Petrochemical Refining Co. advances in COTC technology will not result in the elimination of conventional refining processes but will affect the competitiveness of peer participants in the chemical industry, engineering, procurement and construction contractors, process licensors and technology developers.

The new technology fractionates the barrel of crude oil into its traditional cuts and feeds them to dedicated steam cracker furnaces. The “traditional” refinery is, therefore, converted into a plant that produces a much higher proportion of steam cracker friendly feedstocks, such as LPG and naphtha.

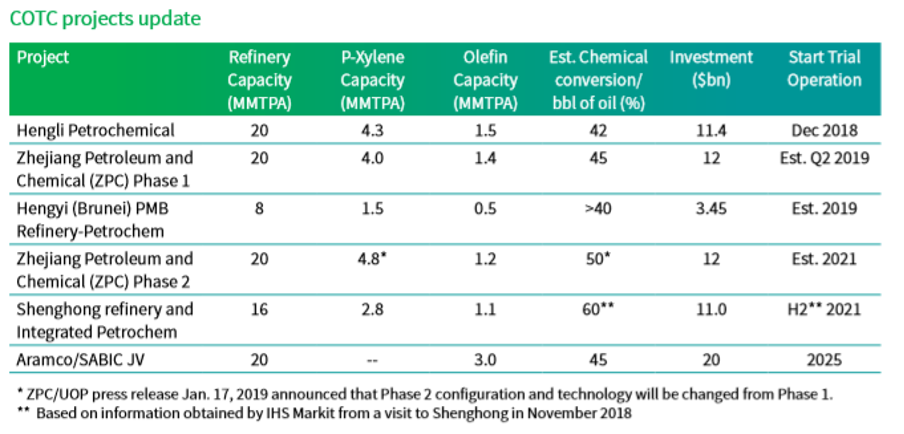

At the time of writing, COTC projects are already on trial with several others in the design phase and scheduled to be delivered in the coming years.

Source: IHS Markit

Conclusion

As with all challenging, disruptive innovations, COTC is expected to substantially impact the global petrochemical industry. COTC architecture requires a reconfiguration of the refinery to upgrade heavy products to chemicals. This goes way beyond the state-of-the-art refinery/petrochemical integration.

COTC’s impact lies in its scalability and high chemical yields which can overwhelm even the largest conventional petrochemical plants. It wouldn’t take more than a few COTC facilities to dramatically alter the world’s petrochemical supply/demand balance.

Awareness of this imminent paradigm shift is imperative. The Onshore Energy market will be required to consider risks and opportunities arising from these new technologies in the construction phase, operational exposures and more flexible economic (BI) limits.

alan taylor

Director, Natural Resources, Charles Taylor Adjusting

Expertise:

Loss Adjuster, Complex Claims Manager, Loss Management Planning, Expert Witness, Mediator, Business Interruption, Refinery and Petrochemical Operations, Construction & Operating Risks

Location:

London